It looks like each few months, there’s a black swan occasion in crypto. In simply the final three years, there’s been Black Thursday firstly of Covid, DeFi summer season 2020, the 2021 bull market, Luna/3AC, after which the FTX collapse. The failure of SVB and the burgeoning banking disaster that’s unfolded over the past two weeks is the most recent unprecedented incident.

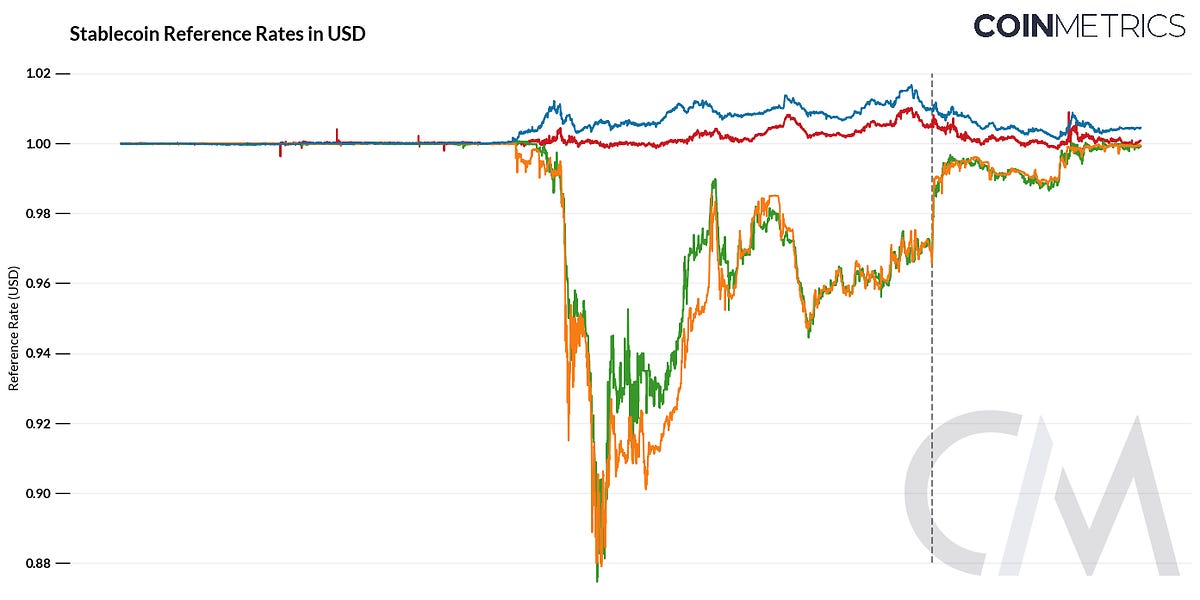

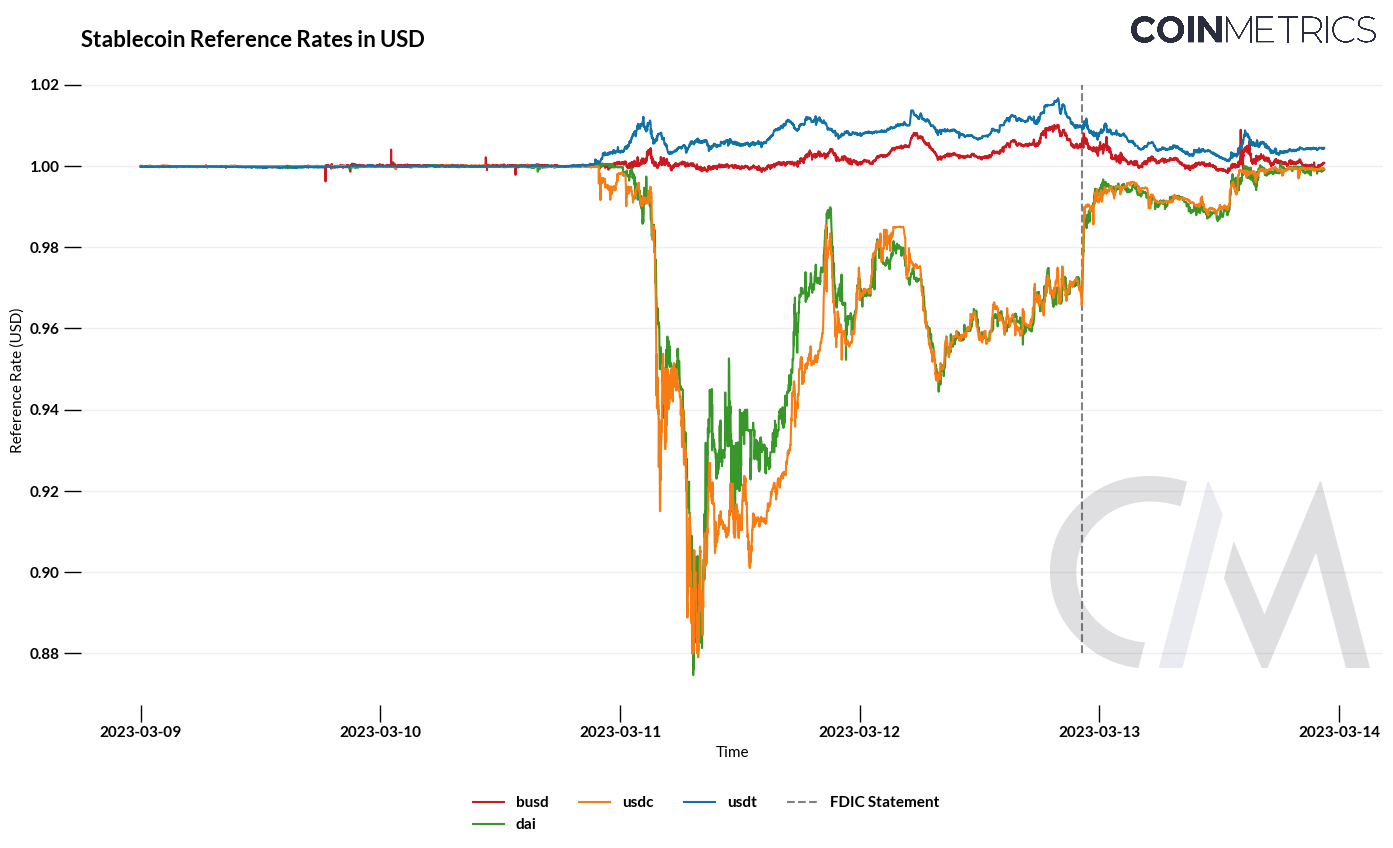

Quickly after the FDIC introduced it had taken over SVB on Friday March 11, USDC – essentially the most trusted stablecoin – started drifting from its peg. It then plunged when Circle revealed it had $3.3bn of money locked up at SVB, after which dropped additional after they halted redemptions earlier than bottoming out at $0.87. Because the weekend went on and with markets closed, USDC’s on-chain value grew to become a proxy restoration fee for SVB depositors, buying and selling sideways under its $1.00 peg. This carried on till the FDIC introduced on Sunday night that every one SVB deposits can be accessible at Monday’s market open.

Because the chart above from Coin Metrics reveals, USDC wasn’t the one stablecoin on the transfer. Dai (aka “wrapped USDC”) mirrored USDC’s value, whereas USDT traded at $1.01+, as buyers have been prepared to pay a premium for stability.

DEX quantity soared on-chain, posting an all-time day by day excessive of $25bn (Uniswap ended at $12bn, whereas Curve had $8bn). MEV-Increase additionally posted an all-time excessive. For a DEX, a depeg – or any volatility – is an efficient factor; there’s no pressure on the system and costs skyrocket. This isn’t true for DeFi lending, the place a depeg might destroy a protocol if danger and volatility usually are not correctly ruled.

Every of the most important lending protocols (Maker, Aave, and Compound) responded shortly with emergency governance actions, and at the moment are discussing long-term modifications to insulate their protocols from failure within the occasion of one other depeg. The impression of those modifications will hinge on whether or not they heed the important thing classes from this newest incident (extra on that later). First, this is how the Huge Three fared:

-

The place they have been: Previous to the USDC depegging, Maker held $2.4bn of USDC (5% of USDC’s circulating provide). Virtually all of this sits in Maker’s Peg Stability Module (PSM), which permits 1:1 trade between Dai and USDC.

-

Through the depeg: As buyers bought USDC (usually for USDT) and pushed down the worth, many USDC holders deposited their USDC within the PSM, minted Dai, after which bought the Dai. This meant that Dai’s value barely lagged USDC’s value, as a result of the PSM enabled the identical promote strain on Dai by permitting 1:1 minting. This resulted in $2bn of further USDC inflows, which Maker is now caught with. MakerDAO governance went into emergency mode, including a 1% payment to the PSM (plugging the opening), decreasing the debt limits on all USDC-based collateral, and growing the debt restrict on USDP (which didn’t endure depegging points). It additionally up to date protocol parameters to permit debt ceiling changes to bypass the Governance Service Module (GSM) Delay.

-

Going ahead: Dai is now extra backed by USDC than it was previous to the depeg. Nobody within the Maker neighborhood is especially completely satisfied about this, however in typical DAO style, they nonetheless can’t agree on a plan to wean themselves off of USDC. More and more, it seems to be like Maker will observe within the course of its founder, Rune Christensen. He additionally prefers essentially the most excessive choice: decoupling Dai from the US greenback to grow to be an unbiased secure forex.

It’s exhausting to sq. this imaginative and prescient with the fact of the right here and now. There’s virtually $6bn of Dai in circulation that desperately desires to be pegged to the greenback. Rune’s concepts don’t appear to acknowledge that Dai is a product that already has market adoption. And proper now, it nonetheless must function inside the confines of its self-imposed USDC straightjacket.

-

The place they have been: Compound is within the midst of transitioning to v3, whereas additionally making an attempt to go multi-chain and claw again some market share from Aave. USDC was hardcoded at $1.00 in its v2 contracts, and Compound solely makes use of it because the borrowing asset in v3.

-

Through the depeg: The Compound v2 Pause Guardian (a multisig) halted USDC provide transactions, whereas persevering with to permit all borrowing. It didn’t pause Dai provide transactions regardless that it mirrored USDC’s fall, probably as a result of the protocol tailored to its value decline as a result of it was not hardcoded.

Notably, Gauntlet really useful pausing borrowing for all belongings, a way more aggressive step that was not carried out. Their concern targeted on Compound customers who have been recursively borrowing – concurrently supplying a stablecoin whereas additionally borrowing a stablecoin. Given the excessive loan-to-value ratio (LTV) of stablecoins and their value correlations, merchants are in a position to make a levered guess whereas additionally farming COMP. The most important danger of this exercise in the course of the depeg got here from an tackle that equipped 20.7m USDC and borrowed 17.1m USDT.

Presumably, this was a leveraged guess to quick USDT. That was not the right guess following the USDC depegging, however with the worth hardcoded at $1.00, this place was protected.

-

Going ahead: All eyes are on v3 and Compound’s enlargement to different chains, with Arbitrum and Optimism up first. Compound didn’t take any danger mitigation measures on v3 in the course of the depegging occasion, as a result of “Compound v3 options an upgraded danger engine”. On v3, solely USDC is borrowable, so there was no danger of unhealthy debt accruing as a result of USDC will not be used as collateral.

-

The place they have been: Aave has all the time been essentially the most aggressive lending participant, whether or not it’s by way of advertising, including new belongings, or increasing to new chains. It launched its v3 six months earlier than Compound, and was additional alongside within the deployment course of; v3 was working stay on Avalanche, Arbitrum, Optimism, Polygon, and Mainnet. Whereas not but carried out on all chains, v3 additionally options E-Mode (effectivity mode), which permits greater borrowing energy for belongings with correlated costs.

-

Through the depeg: USDC was not hardcoded to $1.00, so the protocol’s oracle immediately registered the declining value of the more-than 1 billion USDC deposited into Aave. On v2, with a LTV ratio of 85%, the protocol would solely tackle losses if USDC dipped below $0.85 and didn’t stabilize. So whereas the Aave battle room debated whether or not to pause v2 on Ethereum (the biggest market), it finally didn’t and USDC’s peg ultimately recovered.

Exterior of Ethereum, there have been points: Aave incurred unhealthy debt and needed to take emergency motion. This was for 2 causes. First, there was much less USDC liquidity on smaller chains, with most of it bridged USDC (versus native). Second, Aave v3 on these smaller chains had E-Mode enabled. This enables borrowing of as much as 97% of stablecoin collateral and has a liquidation threshold at 97.5%, so there’s a really tight band for wholesome liquidations.

As the worth of USDC dropped, many recursive stablecoin debtors ought to have been liquidated (when USDC hit $0.97), however most weren’t – USDC liquidity was crumbling so it wasn’t interesting to liquidate (particularly with a low liquidation penalty). As the worth of USDC continued to drop, the protocol missed the window for wholesome liquidations (the place the worth liquidated and returned to the protocol exceeds the excellent debt that’s paid off). Avalanche was hit worst worst, incurring virtually $300k of unhealthy debt. This prompted the Aave Guardian to freeze the USDC, USDT, Dai, Frax, and Mai markets on Aave v3 Avalanche.

-

Going ahead: The Avalanche markets have been unfrozen earlier this week, with plans for the availability caps to be drastically diminished. And now, Aave governance is discussing what changes to make to E-Mode, which is resulting in a frank dialogue on what precisely is the goal use case for E-Mode. The primary downside in the course of the depeg was that a number of the belongings in E-Mode depegged collectively (USDC/Dai) whereas others didn’t (USDT). E-Mode leaves a protocol vulnerable to a depegging incident, which is by nature exhausting to foretell. Aave has but to cross any modifications to E-Mode, however the present neighborhood consensus appears to be to cut back the LTV ratio for stablecoins in E-Mode to insulate the protocol in opposition to the chance of a depeg. Any adjustment to E-Mode parameters will result in important liquidations if positions usually are not unwound earlier than the change is enforce.

First, recursive borrowing might not be well worth the heightened danger. Borrowing and supplying the identical stablecoin will not be dangerous to the protocol – though we do query its utility to the protocol; the larger danger to protocol solvency is from customers that concurrently provide one stablecoin and borrow one other. Recursive borrowing is worthwhile for the consumer due to protocol or chain rewards, and protocols prefer it as a result of it might juice its income (E-Mode on Avalanche yielded virtually $2.5m final 12 months). Is the income and consumer development sufficient to justify the added danger? A potential future affect on the reply often is the emergence of the ETH liquid staking derivatives (LSD), which can fully upend the lending market. Having a system (like E-Mode) that might effectively handle a number of LSDs as collateral could possibly be very interesting to debtors.

Second, USDC might grow to be extra entrenched into lending protocols. It’s advanced to handle a number of stablecoins in a shared lending pool. As extra lending strikes into remoted swimming pools, these will probably include a single borrowable asset (like Compound v3). You possibly can have a ETH-USDC, ETH-Dai, ETH-USDT pool, however protocols might drift in the direction of a most popular stablecoin as to not siphon liquidity. Aave’s E-Mode would have much less insolvency danger if it solely included USDC-backed stablecoins (like Dai and Frax).

Third, a governance system and neighborhood that may reply in actual time is essential to making sure sufficient danger administration. DeFi OGs will recall the confusion and panic in Maker governance within the months following Black Thursday in 2020, when Dai constantly traded above its $1.00 peg. These DeFi days are over. Not like in 2020, there was a swift response and lively dialogue amongst a variety of stakeholders at Maker, Compound, and Aave following the depeg. Some might imagine that DeFi should prioritize governance minimization, however for a lending protocol governance is an unavoidable actuality, given the necessity to steadiness capital effectivity and protocol solvency.

It was not a flawless weekend for DeFi, however the quickness of the governance response underscores how far off-chain coordination in DeFi has come.

Particular due to Nick Cannon, Luigy Lemon and Ross Galloway for inspiration and suggestions on this put up.

-

mevnomics.wtf Hyperlink

-

Coinbase so as to add Uniswap and Aave to L2 Base Hyperlink

-

Information and evaluation on DEX quantity over previous 7 days Hyperlink

-

The Espresso Sequencer goals to decentralize rollup sequencers Hyperlink

-

Lido to permit ETH withdrawals “in mid Might” Hyperlink

-

Idex v4 to launch on Might 22 Hyperlink

-

ARB airdrop Dune dashboard from Blockworks Hyperlink

That’s it! Suggestions appreciated. Simply hit reply. Written in Nashville, the place spring has sprung! I’ll be in Austin the week after subsequent. Attain out in the event you’re round.

Dose of DeFi is written by Chris Powers, with assist from Denis Suslov and Monetary Content material Lab. Caney Fork, which owns Dose of DeFi, is a contributor to DXdao and advantages financially from it and its merchandise’ success. All content material is for informational functions and isn’t supposed as funding recommendation.

{kind=link}